Download Entire report

Pay $4.99The global semiconductor market size reached at $597.3 billion in 2023 and is expected to grow at a CAGR of 7.1 % to reach around $1107.3 billion during the forecast period 2024-2033.

The trend is on enhancing supply chain resilience to the volatility of semiconductors and guaranteeing end-to-end transparency to improve forecasting and demand management, any disruption in supply chain significantly impacts the global economy

With the semiconductor industry expected to expand and carbon emissions expected to double by 2030, government investments and sustainability also took center stage at SEMICON west; this can be accomplished by enhancing digital lifecycle collaboration within FABS and increasing productivity through advanced analytics (ML & AI)

The proliferation of Gen AI-based apps and use cases for manufacturing support and design will revolutionize the way factories' present automation operates. This will cause a significant change in the way the industry shapes and adjusts to this new reality

Since it can replicate the complete fabrication process, manufacturing workflows, and a variety of use cases and models to increase productivity and efficiency, digital twins show off enormous promise for the semiconductor industry

The advancement of sophisticated manufacturing techniques like EUV lithography and 3D stacking holds potential to augment the functionalities of semiconductors. Electronic gadgets that are more compact and energy-efficient are made possible by these advancements, which make it possible to produce chips that are powerful & smaller

The semiconductor business has a great deal of potential as a result of the growth of edge computing and the spread of IoT devices. Due to the need for processors with high computational capacity and low latency for edge computing, semiconductor producers now have more opportunities to develop specific products for this new paradigm.

For the semiconductor ecosystem to overcome obstacles and spur innovation, cooperation in design, production, and testing will be essential. Supply chains become more robust and resilient by enhancing industry collaborations and knowledge sharing

Companies may see revolutionary improvements in processing speed and power as they increase their investments in quantum computing. Furthermore, the price of utilizing quantum computing may go down in the future. Companies that design and manufacture semiconductors should be patient in waiting for a return on investment

1. Industry Overview

2. Industry Market Size

3. Industry Outlook

4. Industry Trends

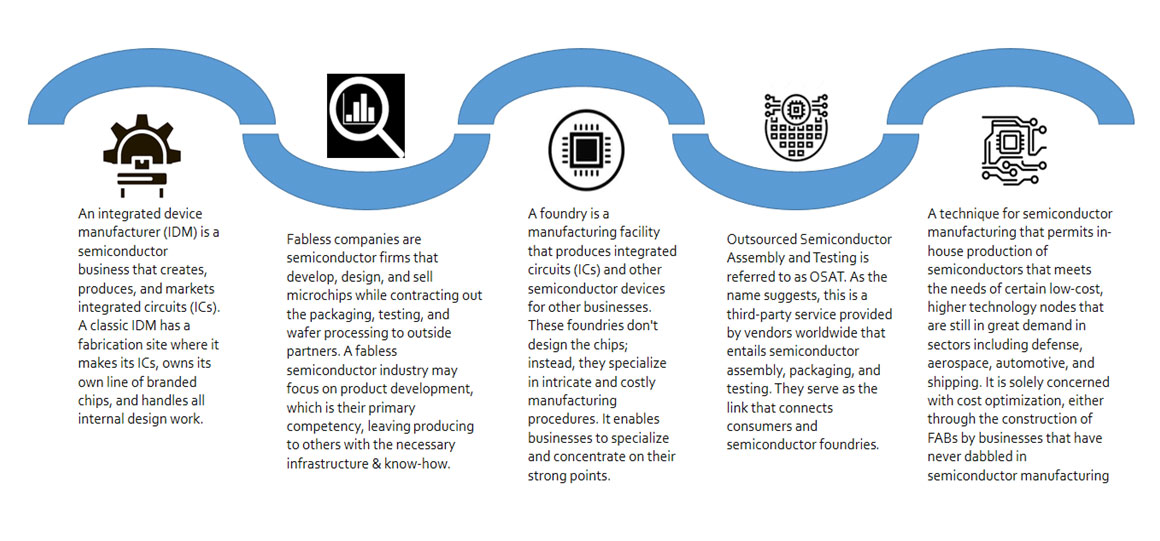

5. Industry Business Models

6. Cost Insights

7. Opportunities and Challenges

8. Competitive benchmarking

9. Company Analysis(1/3)

10. Company Analysis(2/3)

11. Company Analysis(3/3)

12. Regional Insights- India

13. Regional Insights- USA

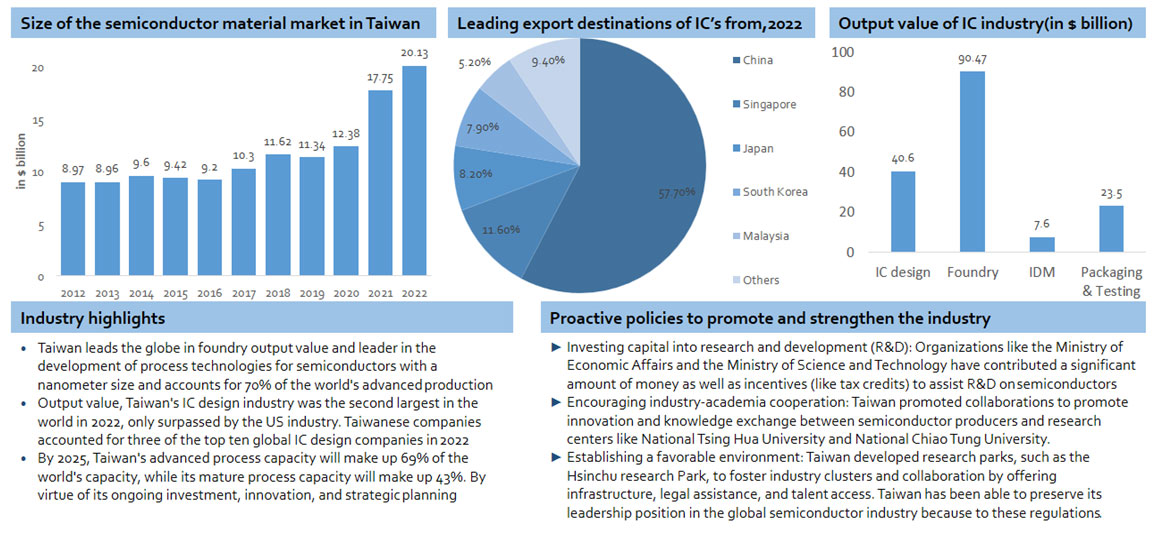

14. Regional Insights- Taiwan

15. Import & Export insights

16. SWOT Analysis

Download Entire report

Pay $4.99